Since returning to office in January, Donald Trump has taken a radically aggressive stance on global trade. He named 2 April “Liberation Day” and announced sweeping reciprocal and protective tariffs targeting every major trading partner.

Although tariffs had long been discussed as a cornerstone of the US administration’s policy, few analysts expected the enacted measures to be so severe. As a result, markets were caught off guard, with little of the impact priced in.

While some analysts expected bold rhetoric, few anticipated such severe execution. The baseline US import tariff was set at 10% (effective 5 April), but for what the administration deemed the “worst offenders”, 57 countries, the penalties were far higher:

- 20% for the European Union

- Up to 49% for Cambodia

- And for China, an extraordinary 104% import levy went into effect on 9 April

Framed by the Trump administration as a justified response to counteract the US trade deficit, the tariffs have instead triggered widespread retaliation and global financial instability.

China responded with a 50% counter-tariff, raising its effective levy on US goods to 84%. As of late April, Chinese exports to the US face tariffs as high as 245%, while Beijing has retaliated with a 125% charge on American imports.

Markets reacted swiftly. On 4 April, the US stock market lost over $2.5 trillion in value. Global markets followed, wiping out an estimated $10 trillion – a sum equivalent to more than half of the GDP of the European Union.

Perhaps more than the equity market losses, it was the sharp sell-off in US Treasuries that ultimately forced the administration to respond. Demand for government bonds collapsed, and the traditionally safe Treasury market came under pressure, signalling a broader, more alarming loss of confidence in the US economy. Key analysts, bankers and institutional investors were raising the alarm, warning that the US was on the brink of triggering a recession if immediate action wasn’t taken. By 9 April, the pressure had reached a point where the administration was forced to act – it announced a 90-day suspension of tariffs for all countries except China. US markets briefly rebounded, but the bounce was short-lived.

Today, volatility persists. The tariffs have added fuel to the fire of already unstable global markets, driven by geopolitical tensions, climate instability, inflationary pressures and broader systemic risk.

In this article, we assess how these US tariffs may impact real estate markets in resort-driven destinations shaped by international demand. We are not going to spend too much time analysing the effects of these tariffs on broader economic dynamics, as they follow well-established macroeconomic principles that have already been widely discussed. Instead, after a brief look to set the stage, we will shift our focus to the more specific implications for overseas resort property markets, with Mallorca as our central case study.

Acknowledging Broader Economic Forces and Complexities of Market Dynamics

While this article focuses on projecting property prices based on GDP levels, it’s worth briefly acknowledging the broader economic forces at play. Tariffs typically increase input costs across the construction sector, putting upward pressure on build prices and potentially on new home prices. At the same time, inflationary effects may well be offset by declining economic activity and a slowdown in demand, which tends to have a cooling effect on pricing. Other market dynamics include interest rate movements, currency shifts, and bond market volatility but the way these forces play out varies widely across countries, and their effect on property markets is virtually impossible to model with precision.

The divergence in central bank responses makes this even clearer. Following the US tariffs, the Bank of England is expected to accelerate rate cuts (source: Reuters), while the same policy shock has complicated the European Central Bank’s roadmap to lower interest rates (source: Euronews), a reminder of just how fragmented and unpredictable these dynamics can be.

Given the huge complexity involved in modelling these macroeconomic effects across multiple destinations, we have instead focused on the clearer signal provided by the metric of real GDP. For both historical and forecasted GDP levels, we have drawn from the IMF’s World Economic Outlook Report – widely cited for its credibility and the sophistication of its modelling.

International Resort Markets vs. Domestic Markets

International resort property markets, such as Mallorca, Phuket, and the Algarve, tend to attract wealthier, internationally mobile buyers. Many purchases are for second homes, lifestyle assets, or long-term investments, rather than primary residences. As a result, overall transactions in these markets exhibit a substantially lower ratio of leverage to cash. Because demand is often driven by lifestyle appeal, capital diversification, and discretionary wealth, they are less exposed to domestic economic cycles or credit conditions. These characteristics generally allow them to weather global downturns with greater resilience, unless distorted by overbuilding or speculative excess, as seen in past cycles in markets like Dubai.

How to Model the Impact on the Mallorca Property Market

Because there are so many overlapping dynamics in real-world economic modelling – from interest rates and inflation to currency shifts, fiscal policy, and consumer sentiment – all of which would need to be applied across the full set of countries that make up Mallorca’s international buyer base, any attempt to build a precise forecast for the island’s property market is ultimately futile.

Instead, the most sensible approach is to focus on the most important macroeconomic indicator, GDP, and use credible forecasts from a globally recognised body – we have used the IMF – to estimate the likely contraction (or growth) in the economies of Mallorca’s primary buyer countries.

By comparing these GDP projections to the actual contractions recorded during the Global Financial Crisis – the most appropriate historical analogue – and assessing how Mallorca performed during that period, we can arrive at a grounded, proportional sense of how the island’s property market is likely to be affected.

Though our core model focuses on GDP as a clear and consistent proxy for macroeconomic pressure, it is hugely important to note one key difference between the current environment and the post-GFC period: there is no evidence of a systemic credit squeeze. We return to this point later in the article, as it has important implications for how demand may translate into transactional activity.

Our Methodology

To assess the likely impact of global tariffs on the Mallorca property market, we’ve used a straightforward, comparative approach:

- Identify the main international buyer countries for Mallorca, based on official transaction data.

- Source GDP forecasts for 2025 from a single, reputable forecasting body to ensure consistency – in our case, the IMF.

- Apply each country’s market share (as a percentage of foreign transactions in Mallorca) to calculate a weighted average GDP projection for the overall buyer pool.

- Identify the GDP contraction experienced by Mallorca’s primary buyer countries during the Global Financial Crisis, and calculate a weighted average based on their share of property transactions.

- Compare the weighted average GDP contraction during the GFC to the current GDP forecast, to estimate the relative level of economic pressure and its likely impact on property prices in Mallorca.

Foreign Buyer Distribution for Mallorca

According to the Majorca Daily Bulletin (April 2025), foreign buyers accounted for 32.6% of property purchases in the Balearics. A separate report from the same publication (October 2023) provides a breakdown by nationality with Germans representing 38% of foreign buyers, Britons 25%, and Americans 13%.

Share of Total Transactions by Buyer Nationality

- Germany: 12.39%

- United Kingdom: 8.15%

- United States: 4.24%

- Other countries (Eurozone): 7.86%

- Spain (domestic): 67.4%

Note: The remaining 24% of foreign buyers were not broken down by nationality in the source data. For modelling purposes, we have allocated this share to other Eurozone countries.

Modelling the Pressure on Buyer Economies

To quantify the level of economic pressure likely to affect property demand in Mallorca, we constructed a weighted average GDP forecast using the IMF projections for 2025, see table below, and our breakdown of buyer nationalities as given above. Each country’s GDP forecast was weighted according to its share of total property purchases.

This approach provides a proportional view of how strongly macroeconomic conditions are likely to influence overall demand. The result is a weighted average GDP forecast of +2.02% (see appendix for calculation).

This figure reflects the mix of strong domestic growth – Spain (2.5%) – and weaker forecasts from key international markets such as Germany (0.9%), the United Kingdom (1.1%), the United States (1.8%), and other Eurozone countries (0.8%). It provides a clear, proportional estimate of the economic climate facing Mallorca’s property sector in 2025, based on GDP projections published by the International Monetary Fund (IMF), April 2025 World Economic Outlook, see below:

IMF GDP Projections for 2025

| Country / Region | 2025 GDP Forecast (%) |

|---|---|

| Spain | 2.5 |

| Germany | 0.0 |

| United Kingdom | 1.1 |

| United States | 1.8 |

| Other countries (Euro Area proxy) | 0.8 |

Note: data is based on statistical information available through April 14, 2025.

Even under JP Morgan’s downside scenario (their prediction is based on a 10% universal tariff and a 110% tariff on China) – where tariffs reduce global GDP by as much as 1% – the outlook for Mallorca remains comparatively strong. The IMF’s baseline projection for 2025 is +2.8%, and our weighted GDP growth forecast for Mallorca’s primary buyer economies stands at +2.02%. That’s not just positive – it’s historically resilient when compared to the contraction experienced during the GFC, which we will explore later.

US Performance Figures for Quarter One 2025

The U.S. economy contracted by 0.3% in the first quarter of 2025 (Wall Street Journal, April 2025), largely driven by front-loaded import activity and broader uncertainty surrounding the Trump administration’s tariff policies. Whether or not a second quarter of contraction will follow – which would meet the standard definition of a technical recession – remains to be seen. For now, the IMF’s full-year projection still expects the U.S. to grow by 1.8% in 2025, reflecting a possible rebound in the second half of the year.

Contractions: GFC vs. Projections for 2025

To understand how serious the current global pressures might be for Mallorca’s property market, we look back at the Global Financial Crisis – the last sustained period of global economic contraction.

In 2009, our key Mallorca buying countries experienced sharp and synchronised economic contractions.

| Country / Region | 2009 GDP Contraction (%) |

|---|---|

| Spain | -3.7% |

| Germany | -4.7% |

| United Kingdom | -4.9% |

| United States | -2.6% |

| Other countries (Euro Area proxy) | -4.1% |

Based on the IMF data above, we calculated a weighted average GDP contraction of –3.91% (see appendix for calculation) across Mallorca’s primary buyer base that year.

By contrast, for 2025, the weighted average GDP forecast for those same countries for 2025 is +2.02%. This marks a swing of nearly six percentage points – a significant improvement in the macroeconomic backdrop compared to the post-GFC environment.

The Resilience of Mallorca’s Property Market

Mallorca’s ability to weather shocks is rooted in deeper structural features that have remained consistent across decades of global downturn and crisis. These characteristics help explain why the island’s property market has historically shown greater stability than other regions, and why it recovered more quickly after the Global Financial Crisis.

The Mallorca and Spanish Property Markets: Performance During and After the GFC

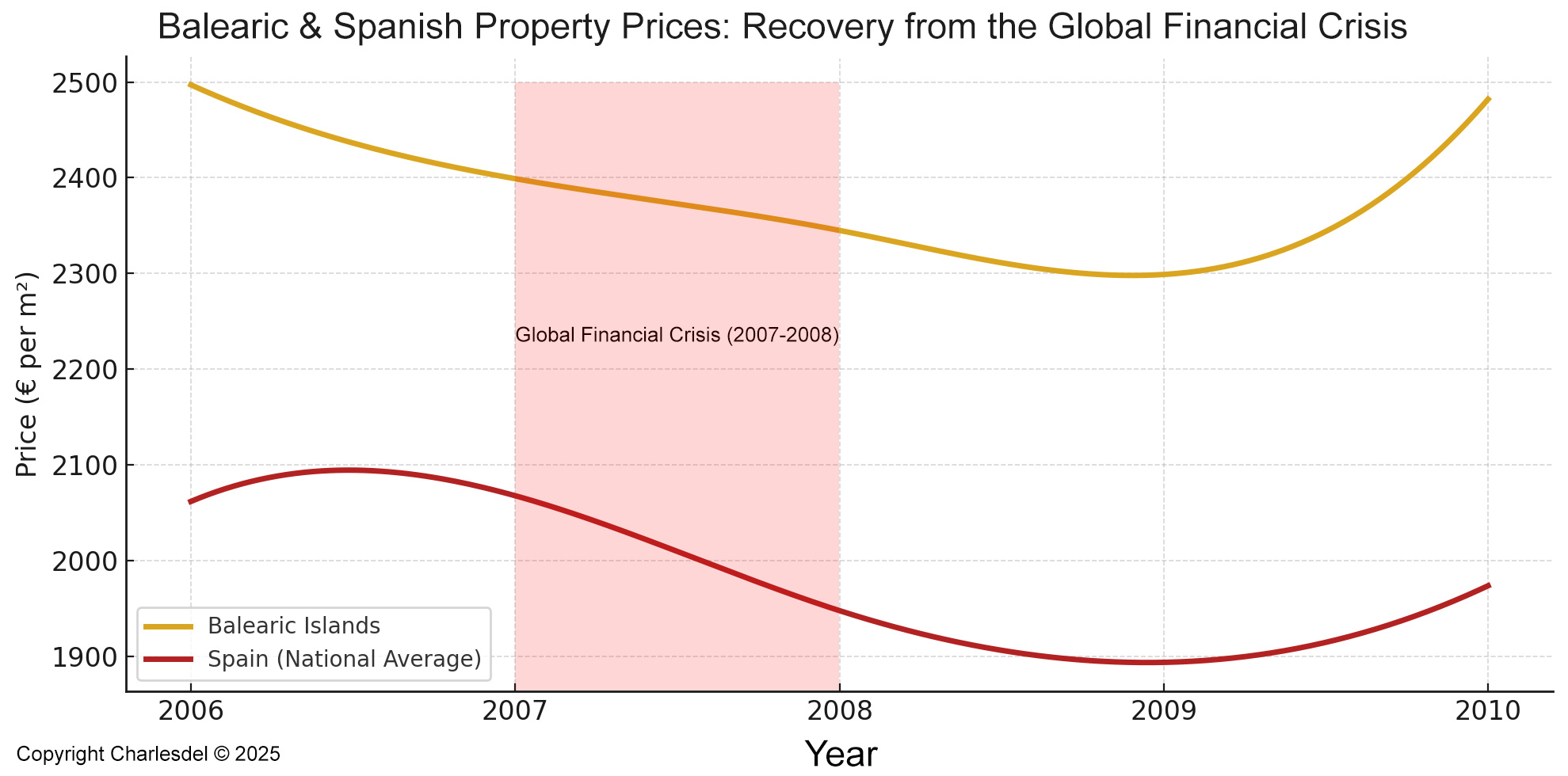

Unlike many domestic markets that suffered sharp corrections during the GFC, Mallorca’s downturn was modest. Prices did decline in 2007 and 2008, but by 2009, Idealista data shows that a recovery was already underway – driven largely by sustained international demand and a strong tourism base. The graph below illustrates how prices in the Balearic Islands rebounded more quickly than the national average.

Several factors contributed to this resilience which still hold true today. The most notable include:

- High proportion of cash purchases – driven by lifestyle buyers, second-home owners, and long-term investors, particularly in the luxury segment

- Tourism-led demand – sustained by a robust year-round tourism sector

- Strict planning and zoning restrictions – which limit supply and support long-term pricing stability

These characteristics give the Mallorca property market a fundamentally different profile from those more dependent on domestic credit and wage-driven affordability. Even in the face of global uncertainty, it is better positioned than most to absorb shocks – not because it is immune, but because its foundation is structurally stronger.

Even in the face of global uncertainty, Mallorca’s resilience has been demonstrated time and again – not only during the GFC, but also through the European debt crisis, Spain’s austerity programme, the COVID-19 pandemic, and most recently the Ukraine war and inflation spike. This consistency reflects a market less dependent on domestic credit cycles or wage-based affordability, and more influenced by internationally driven demand for luxury lifestyle and investment properties. While its reliance on tourism introduces a degree of vulnerability – particularly in the face of prolonged global disruption – Mallorca’s reputation as a leading destination for luxury lifestyle property has steadily strengthened. Built over decades of cumulative brand equity, that reputation has helped the market absorb shocks and maintain long-term stability.

Perspective Matters

It’s important to keep the current volatility and broader market downturns in perspective. While U.S. tariffs have introduced real uncertainty into global markets, the conditions today are fundamentally different from those of 2009. Back then, Mallorca’s primary buyer economies experienced a synchronised GDP contraction of –3.91%. In 2025, the weighted GDP forecast for those same countries stands at +2.02% – a swing of nearly six percentage points.

Mallorca is entering this period from a position of strength. Prices in the Balearics are at an all-time high, with a year-on-year increase of +13.9% as of March 2025, according to Idealista. Demand remains healthy, and the buyer base is resilient. Unlike the post-GFC environment, the island is not climbing out of a slump but building on sustained momentum. Despite the significant uncertainties introduced by the tariffs, the data suggests that Mallorca is likely to perform far more strongly than it did during the Global Financial Crisis.

Another very important distinction between the current period and the post-GFC environment is the absence of a systemic credit squeeze. Basel III – the international banking framework developed in response to the 2008 crisis – triggered a sharp contraction in lending when first introduced, but today it no longer acts as a constraint. GDP tells us about economic output – but what about the key conditions that enable a buyer to act? For those requiring finance – though relatively fewer in Mallorca compared to most property markets – the availability of lending is one such condition. And unlike in 2009, that condition remains intact – ensuring continued accessibility to the Mallorca market for buyers who depend on credit.

- High proportion of cash purchases – driven by lifestyle buyers, second-home owners, and long-term investors, particularly in the luxury segment

- Tourism-led demand – sustained by a robust year-round tourism sector

- Strict planning and zoning restrictions – which limit supply and support long-term pricing stability

Timeframe and Market Reaction

The 90-day suspension of tariffs will expire in the early part of Mallorca’s peak holiday season. While it will be too early at that stage to fully assess the impact of U.S. policy, trend indicators such as booking levels, buyer enquiries, and broader sentiment should begin to emerge. By the end of the summer, the overall trajectory is likely to be clearer.

While direct exposure to the U.S. buyer market is limited, American policy remains highly influential. Its economic impact on key European economies, especially Germany and the UK, can significantly affect broader sentiment and purchasing power. In that sense, the path chosen by the U.S. administration will help shape the macroeconomic environment surrounding Mallorca’s core buyer groups.

Update – 16 May 2025 – De-escalation with China

On 14 May, a deal between the United States and China came into effect, significantly reducing the severity of the tariffs introduced in early April. Under the new arrangement, the US now imposes a 30% tariff on all Chinese goods, down from as high as 145%, while China has reduced its levy on American imports to 10%, down from 125%.

While this marks a meaningful de-escalation, the remaining tariffs still represent a substantial increase over pre-crisis levels. US businesses that rely on imports continue to feel the pressure. Walmart, widely regarded as the world’s largest high street retailer, announced yesterday that it will be raising prices this month, explaining that it is unable to fully absorb the increased costs of the 30% import tax.

However, in the context of the Mallorca property market, it is more important to note that the tariff hikes on other US trading partners – including the 20% import duty on goods from the European Union – remain fully in place. These non-China tariffs are far more relevant, given the significantly larger share of buyers from European countries.

More broadly, the abrupt imposition and now partial rollback of tariffs underscore the unpredictability of the current US administration’s economic policy. Even if further relief measures are introduced, volatility remains a defining feature of the present environment. Our modelling, based on weighted GDP forecasts for Mallorca’s key buyer countries, continues to suggest that the island is structurally well-positioned to withstand even the most significant global shocks.

Update – 30 May 2025 – Appeals Court Reinstates Tariffs Amid Legal Turmoil

On 29 May, the U.S. Court of International Trade ruled that President Trump had exceeded his authority under the 1977 International Emergency Economic Powers Act and gave the administration 10 days to revoke the “Liberation Day” tariffs. But on 30 May, the U.S. Court of Appeals for the Federal Circuit temporarily stayed that decision, allowing the tariffs to remain in effect while the appeal is considered (source Reuters).

Markets responded positively to the initial ruling on Wednesday, but gains were modest — analysts had already anticipated legal challenges. That scepticism proved merited following the appeals court’s intervention.

The key point is that reinstatement of the tariffs is only temporary, giving the U.S. administration the opportunity to pursue further appeals through higher courts. These latest legal wranglings illustrate, quite clearly, the level of uncertainty at play, uncertainty over how policy is created, whether it will remain in place, and what its actual effects might be. How can you begin to predict the impact of a policy when you can’t even be sure it will stay intact?

Update – 7 November 2025 – Post-Tariff Mallorca Property Market Impact

Let’s take a quick look what tariffs were applicable to the European Union before the changes introduced by the U.S. administration in April 2025. Until this point, apart from the 25 percent tariff on steel and 10 percent on aluminium, which had been enforced since the 2018 Section 232 measures, there were no general tariffs on EU goods. What changed in April 2025 was the announcement of the universal 10% import tariff a higher 20 percent “reciprocal” rate for EU goods. However, we should note that they were only very briefly enacted, and their collection was suspended within days. They were quickly replaced by a 15 percent framework agreed between Washington and Brussels on 25 July 2025 (source BBC, 27 July 2025). This structure reduced the extreme rates initially threatened but locked in a permanent 15 percent tariff, still far more than the near-zero duties that applied before the dispute began.

Mallorca Property Prices, July–October 2025

Here we take a look at property prices in Mallorca following the tariff changes to see how the market performed. We focus on the period from July to October 2025 – the first continuous window after the U.S. tariffs were reinstated.

| Month | Average Price (€/m²) |

|---|---|

| October 2025 | 5,115 €/m² |

| September 2025 | 5,090 €/m² |

| August 2025 | 5,068 €/m² |

| July 2025 | 5,025 €/m² |

Source: Idealista – average property price for the Balearic region used as a proxy for Mallorca.

So, looking at our time period for post tariff changes, Majorca property prices continued to climb steadily over the four month period, rising from €5,025 /m² in end July to €5,115 /m² by 31st October 2025.

If you find this information useful and plan to share it, please credit us with a link to https://charlesdel.com/

Appendix: Weighted Average GDP Calculation (2025)

Data Sources:

- GDP forecasts: IMF World Economic Outlook, April 2025

- Buyer share data: Majorca Daily Bulletin, April & October 2023–2025

| Country / Region | GDP Forecast (%) | Buyer Share (%) | Weighted Contribution |

|---|---|---|---|

| Spain | 2.5 | 67.4 | 2.5 × 67.4 = 168.5 |

| Germany | 0.9 | 12.39 | 0.9 × 12.39 = 11.151 |

| United Kingdom | 1.1 | 8.15 | 1.1 × 8.15 = 8.965 |

| United States | 1.8 | 4.24 | 1.8 × 4.24 = 7.632 |

| Other (Eurozone) | 0.8 | 7.86 | 0.8 × 7.86 = 6.288 |

Total Weighted Contribution:

168.5 + 11.151 + 8.965 + 7.632 + 6.288 = 202.536

Divide by total buyer share (100%):

202.536 / 100 = ~2.02%

Appendix: Weighted Average GDP Contraction (2009 – GFC)

Data Sources:

- GDP data: IMF World Economic Outlook, October 2010

- Buyer share data: Majorca Daily Bulletin, April & October 2023–2025

| Country / Region | 2009 GDP Contraction (%) | Buyer Share (%) | Weighted Contribution |

|---|---|---|---|

| Spain | -3.7 | 67.4 | -3.7 × 67.4 = -249.38 |

| Germany | -4.7 | 12.39 | -4.7 × 12.39 = -58.233 |

| United Kingdom | -4.9 | 8.15 | -4.9 × 8.15 = -39.935 |

| United States | -2.6 | 4.24 | -2.6 × 4.24 = -11.024 |

| Other (Eurozone) | -4.1 | 7.86 | -4.1 × 7.86 = -32.226 |

Total Weighted Contribution:

-249.38 + -58.233 + -39.935 + -11.024 + -32.226 = -390.798

Divide by total buyer share (100%):

-390.798 / 100 = ~–3.91%