The 2025 Phuket Real Estate Market Report | Trends & Investment Insights

The Phuket real estate market is cash-based and tourism-driven, with foreign buyers playing a dominant role. Unlike mortgage-dependent markets, Phuket’s residential property transactions are mostly cash, contributing to long-term stability.

Many articles briefly mention the relationship between Phuket’s tourism sector and the performance of its residential real estate market. In this article, we more than scratch the surface – by examining data from 2000 onwards, we take an in-depth look at the correlation between tourist arrivals and Phuket’s property market performance. This analysis also highlights how Phuket’s robust tourism sector has consistently demonstrated resilience, quickly recovering from major global economic events that have severely impacted other markets worldwide. Additionally, we explore the cash-based nature of Phuket’s property market, which provides a layer of stability, and compare it with the resort market of Mallorca, where mortgage-driven transactions have led to greater fluctuations in property values.

Tourism may have initially driven demand, but today, many property buyers of Phuket real estate are not tourists; they are purchasing homes to live in permanently or semi-permanently. Some reside in nearby Asian cities and commute easily for weekends, while others, including families and digital nomads, have made Phuket their full-time home.

All major resort destinations in Thailand, particularly Phuket, Koh Samui, and Pattaya, share a common characteristic: the performance of their property markets is closely tied to the strength of their tourism sectors. Most residential properties, excluding affordable housing for local labour forces, are purchased by foreign investors. Overseas buyers typically discover these property markets while vacationing and, after multiple visits, or maybe less, decide to invest.

Thailand’s resort real estate market is dominated by foreign investment, as properties are typically priced beyond the reach of the average Thai buyer and designed to meet international preferences. Developers cater to the styles and price points of foreign buyers, making tourism a key driver of residential property development in Phuket. However, as developers release properties aligned with the preferences of foreign investors, they simultaneously fuel more foreign demand for real estate in Phuket, creating a cyclical relationship between tourism and the property market. While some Thai nationals invest in these markets, they represent a minority. However, a notable exception is Phuket’s luxury villa sector, with developers in 2024 reporting a noticeable increase in transactions involving affluent Thai buyers in premium location such as Bang Tao.

It is no surprise that tourism-driven demand is a defining feature of real estate markets in resort destinations worldwide. The extent to which investors dominate the local market largely depends on whether property prices are beyond the financial reach of the local population. Similar to the resort markets of Thailand, Bali is another prime example of a destination where tourism plays a dominant role in shaping the property market.

Here we focus on Phuket, Thailand’s largest island, which has the country’s most mature and developed resort property market, featuring some of its most exclusive and luxurious residences. Foreign buyers who can afford second homes abroad typically belong to the high-net-worth segment. This is particularly true in the luxury property market, where demand remains strong even during economic downturns.

The Correlation with Tourism

When Phuket’s property market first developed, it followed the trajectory of many emerging markets, experiencing rapid initial growth due to untapped opportunities and new demand. However, its continued resilience and consistently strong performance as it matures over four decades highlight the advantages of its tourism-driven, cash-led market, including:

- The cash-based nature minimises risks of property bubbles and financial crashes due to virtually no leverage.

- Diversification reduces demand volatility with buyers from a range of international markets.

- The large proportion of high-net-worth investors is typically more able to withstand the pressures of economic downturns.

- The development of the branded property sector of Phuket real estate market, starting with the creation of Laguna on Bang Tao Beach by Banyan Group in 1988. Since this date, the island’s branded sector has evolved to become Asia’s leading destination for luxury branded property. This progression has significantly accelerated in recent years with recent high profile branded developments including Tri Vananda, and the Standard Residences

- Phuket developers are tailoring properties to the preferences of high-net-worth international investors, resulting in a cyclical relationship that reinforces the luxury sector.

- Thailand’s well-publicised, long-term commitment to investing in Phuket’s tourism infrastructure, which is closely tied to broader infrastructure development on the island. Phuket’s real estate growth is intrinsically linked to its tourism sector. Continuous investments in tourism infrastructure, such as international hotels, restaurants, and transport links, create a positive feedback loop, drawing in more visitors and driving demand for residential properties, particularly holiday homes and lifestyle investments.

Phuket’s Resilient Real Estate Market

Phuket’s real estate market has shown consistent resilience, quickly rebounding from major global crises, including:

- The 2004 Boxing Day tsunami

- The Dot-Com Bubble collapse and 9/11 attacks (2000–2001)

- The SARS outbreak (2002–2004)

- The Global Financial Crisis (2007–2008)

- The COVID-19 pandemic, with Phuket reopening through the Sandbox program in July 2021

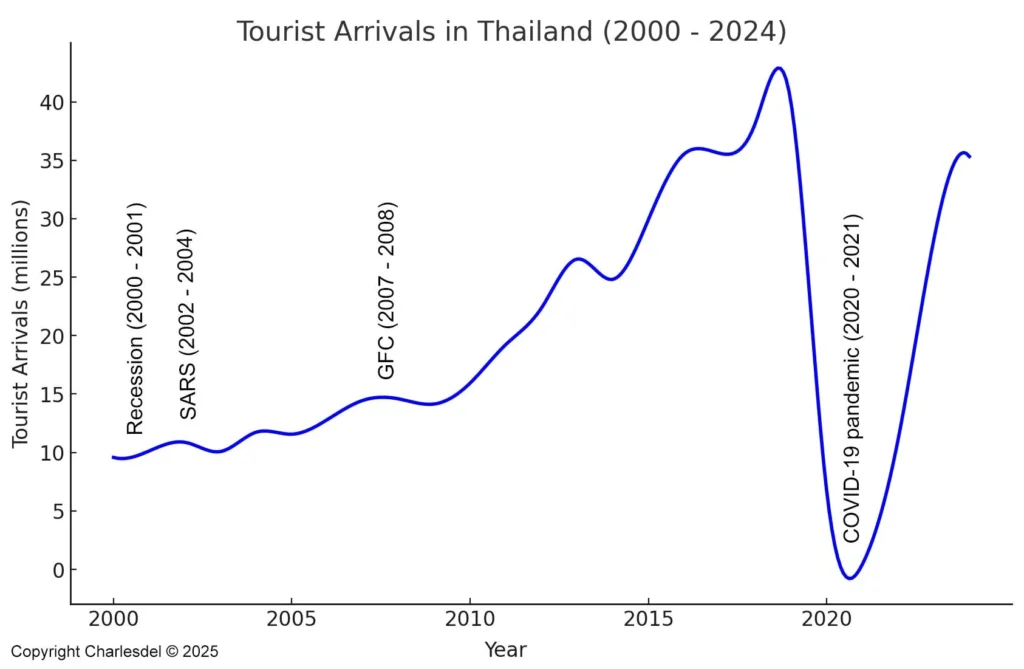

Tourist Arrivals in Thailand (2000–2024)

This graph illustrates the strength of Thailand’s tourism sector, showing how tourist arrivals have consistently rebounded after major global events, the most being the pandemic.

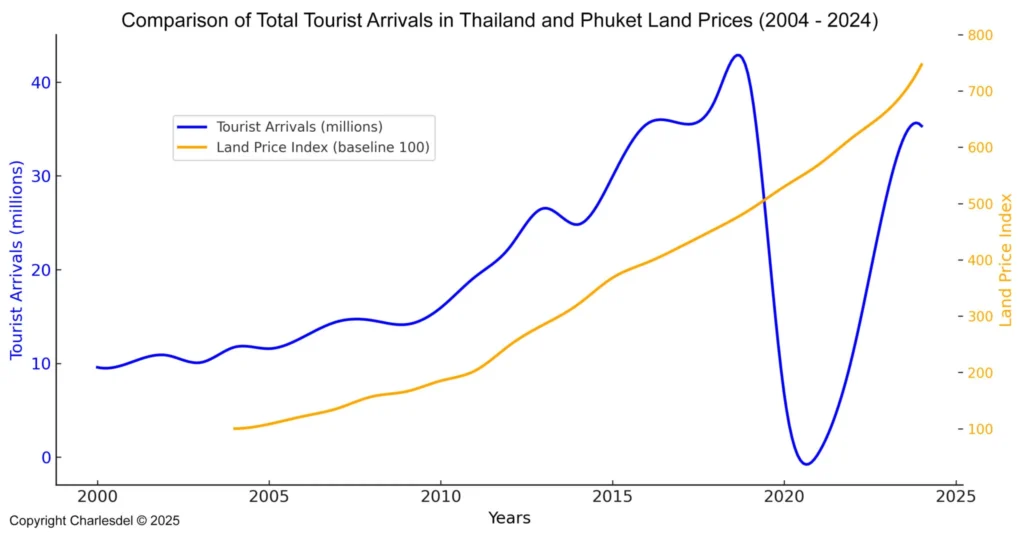

Looking at Phuket’s land prices, a key indicator of property values, we see consistent growth since 2004, even when tourist numbers dropped during the pandemic. Between 2004 and 2024, land prices increased by 647%, averaging an annual growth rate of 10.58%.

Thailand Tourist Numbers and Phuket Land Prices

Additionally, Phuket’s broad international appeal attracts buyers from Asia, Europe, Russia, and beyond. Many are drawn by the island’s pristine beaches, vibrant culture, and modern amenities. For many buyers, purchasing property in Phuket is as much about embracing a desirable lifestyle as it is about potential investment returns.

Phuket’s Cash-Based Market and Its Role in Stability

A key factor behind this resilience is the cash-based nature of the market. Since foreign buyers cannot obtain mortgages from Thai lenders, virtually all purchases – especially in the luxury sector, where foreign buyers dominate demand – are made with cash. This lack of leverage protects the market from economic shifts, such as interest rate changes and stricter lending criteria, which typically impact leveraged markets, thereby providing greater stability.

Comparing to a Leveraged Market: Phuket vs. Balearic Islands

Phuket’s real estate market is primarily cash-based, reducing financial volatility, while the Balearic Islands rely more on mortgage-driven purchases, making them more susceptible to economic downturns.

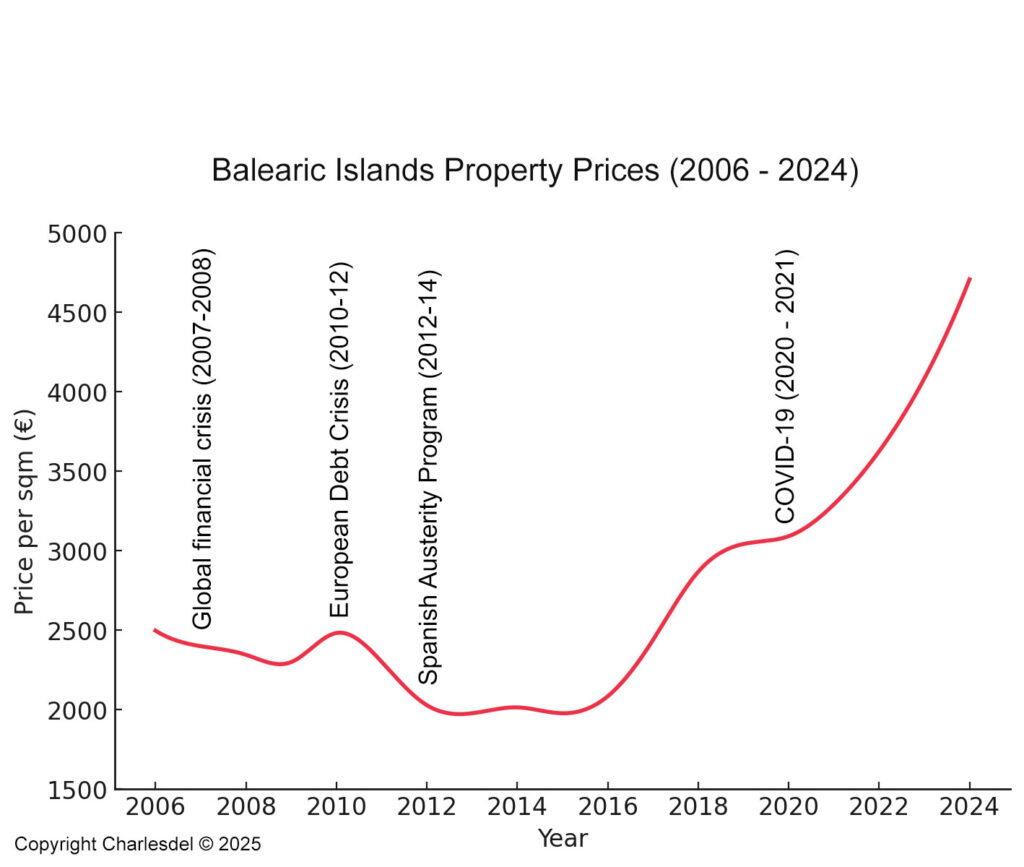

To illustrate this point, we compare Phuket’s market with that of the Balearic Islands. Both are resort destinations with a high percentage of foreign buyers. However, in Spain, foreign investors can easily obtain mortgages, creating a market susceptible to property bubbles and subsequent crashes as economic conditions tighten. The graph below highlights the direct correlation between economic downturns and property price declines in the Balearics, whereas Phuket’s market has remained consistently stable.

Balearic Islands Property Price Trends (2006–2024)

Despite initial disruptions, property prices remained stable during the COVID-19 pandemic, as travel restrictions were brief, covering a three-month period, and borrowing conditions were not significantly impacted.

Market Recovery Post COVID-19

Phuket’s real estate market rebounded sharply after travel restrictions were lifted. In 2022, 149 villas were sold across all nationalities, exceeding the pre-pandemic figure of 131 for 2019, and a 338% increase from just 34 units in 2021 (source: Bangkok Post). By 2023, sales surged further, with CBRE reporting a record 400 resort villa transactions- quadrupling the annual average.

Condominium sales followed a similar trend. The REIC recorded 1,966 condo transfers in 2022, compared to 1,425 in both 2021 and 2020, and 2,163 in 2018.

For 2024, while final figures are not yet widely available, the performance will be impressive with Phuket villa sales reaching 787 in the first half of the year, compared to 403 in the last six months of 2023. The market’s strong recovery following the pandemic was enabled not only by the resurgence of demand led by tourism but also by critical continued investment in Phuket’s infrastructure.

Phuket Infrastructure: A Critical Role

Phuket’s long-term real estate growth is enabled by continuous infrastructure development. Major projects, including airport expansions, road upgrades, and expressway plans, have enhanced accessibility, fuelling tourism and property demand.

The island’s international airport connects it to major global cities, and ongoing expansions aim to boost passenger capacity from 12.5 million to 18 million annually.

Investment in road networks has also been significant, with recent upgrades to Highway 402 and plans to expand Highway 4027 to four lanes by 2026. By 2030, a proposed expressway linking Patong Beach to Phuket Airport will further improve connectivity.

Decades of infrastructure development, notable milestones including the completion of the Sarasin Bridge in 1967 and the opening of Phuket International Airport in 1984, have propelled the island’s transformation into a world-class destination for high-end tourism and property investment. With Thailand welcoming 35.32 million international tourists in 2024, the government’s continued investment in infrastructure will further support Phuket’s long-term real estate market stability.

Update May 2025

2024 Year-end Performance

According to Knight Frank Thailand, 2024 marked the strongest year for Phuket real estate in over a decade. On the back of a thriving tourist sector, with over 13 million visitors to the island in 2024 (source: Bangkok Post), both condominium and villa markets recorded sharp increases in supply and sales. While both asset classes saw strong growth, condos outpaced villas by roughly a factor of three, suggesting a shift in buyer preferences.

A record 1,263 new villas were launched in 2024, a 51% rise year-on-year, with Bang Tao, Cherng Talay and Phru Champa among the most active zones. Condo launches surged as well, with over 10,000 new units entering the market, led by developments in Bang Tao.

Sales volumes reflected this growth: 573 villas were sold, up 18% on the year, while condo transactions exceeded 6,000 units – a 60% increase. Demand remained strongest among Russian and Chinese buyers, who continue to favour Phuket for both lifestyle and rental yield potential. Bang Tao, Rawai and Cherng Talay were highlighted as top rental locations.

Condo pricing held steady, averaging 140,000 THB per sqm, while villa prices moved higher as developers focused on larger plots and more functional layouts. With limited land available in prime west coast areas, new supply is now pushing into hillside zones such as Bang Jo and Phru Champa.

US Tariffs, Uncertainties and Economic Downturns

Recent developments in 2025, most notably the economic uncertainty introduced by aggressive new US tariffs proposed in April, have added a fresh layer of volatility to global markets and led to downgraded GDP forecasts for many countries, including Thailand.

Compounding this macro-level volatility is possibly the most significant uncertainty facing foreign buyers: the legal options for property ownership. While the law itself has not changed, the government is now strictly enforcing it. Most notably, nominee arrangements are explicitly prohibited.

Not surprisingly, many prospective overseas investors are somewhat bemused. For years, it was widely accepted that a freehold villa could be acquired via a Thai company structure, with local shareholders often arranged by legal firms. These companies were typically set up quickly and used as a workaround to enable foreign ownership.

That situation has now changed drastically. Thai law is being enforced to the letter, and any company used to hold a villa must be fully compliant, with Thai shareholders who have a genuine interest in the company, which must have been established with the clear intention of operating as a profit-making entity.

At the same time, in the first half of 2024, the Thai government announced proposals to extend the maximum lease term from 30 to 99 years. Whether this will ever become law remains uncertain, but many prospective foreign investors are putting their plans on hold in the hope of improved ownership options in the future.

Read more about how Phuket’s property market is positioned to navigate this new era of volatility.