Since Phuket International Airport commenced international flights in 2007, the island has steadily evolved from a little-known beach destination into a world-renowned resort market, and in recent years, into Asia’s leading location for branded residential property. Today, Phuket offers a unique blend of lifestyle appeal, international infrastructure, and long-term investment potential.

There is one key driver for the property market: tourism. But the remarkable performance of the tourism sector has only been enabled by sustained investment in infrastructure. Neither functions in isolation. Without government investment in airports, hospitals, and roads, tourism could not have scaled. And sustained tourist demand is undoubtedly the facilitator of consistent real estate growth. Working in tandem for over two decades, these two factors have been the catalyst for the island’s transformation into a globally recognised centre for luxury lifestyle property investment.

Here we provide a concise overview of the Phuket property market: how it works, who’s buying, where the demand is going, and how long-term fundamentals have supported price growth even through periods of global volatility.

For detailed structural analysis and current market trends, see our 2025 Phuket Real Estate Market Report.

Why Phuket’s Property Market Stands Apart

Phuket’s real estate market operates very differently from Thailand’s domestic residential sector. While Bangkok and other urban markets are shaped more by domestic income, credit cycles, and mass-market condo supply, Phuket is dominated by international buyers, lifestyle investors, and cash transactions.

Roughly 60–70% of residential property purchases in Phuket are made by foreign nationals. Most of these buyers fund their purchases with cash, as Thai banks do not lend to foreigners for property purchases in Thailand. This gives the market a unique resilience: it is far less exposed to interest rate volatility, mortgage restrictions, or short-term economic dips in Thailand’s domestic market.

A significant proportion of buyers, both foreign and Thai, fall into the high-net-worth category. Even when financing is available (typically only to Thai nationals), many buyers do not rely on credit to complete their purchases. This further insulates the market from the effects of tighter lending conditions or broader economic uncertainty.

Buyers are also often looking for lifestyle-led assets, not pure capital appreciation or speculative plays. Some are acquiring holiday homes with flexible rental options, while others are seeking second homes, retirement bases, or family residences for semi-permanent living. This demand structure helps explain why Phuket property values have shown greater stability through global shocks such as the 2008 financial crisis and the 2020–2022 pandemic years.

Ownership Options for Foreign Buyers in Phuket

Foreigners cannot directly own land in Thailand, and standard lease terms are limited to 30 years. However, several legal structures allow international buyers to acquire property in Phuket, depending on the type of asset:

- Freehold condominiums: Foreigners can own up to 49% of a registered condo development on a freehold basis, with title registered in their own name.

- Leasehold: For villas and ‘regular’ apartments (which are not classed as freehold condominiums), long-term leases (up to 30 years) are a common way to secure usage rights over land or property. Sometimes developers offer renewable leases, but the security of the renewals needs to be scrutinised.

- Thai company ownership: In some cases, land may be held through a legally compliant Thai company. The law itself has not changed for many years, but in 2024 the government began strictly enforcing the letter of the law. This prohibits the use of nominees for the Thai shareholders, and the company must have been created with the intention of generating a profit, not simply acting as a holding vehicle for the land.

- Villas within condominium projects: A small number of villas are available with condo licences, allowing foreigners to own villa units freehold via shared land co-ownership.

For a full explanation of legal structures, ownership rules, and tax implications, see our guide to Legal & Tax in Thailand.

Where Buyers Are Coming From

Russian and Chinese buyers have been the most active since 2022, with Russians in particular showing strong preference for west coast villas in areas with access to international schools and high-end retail. Chinese buyers tend to favour condominiums as holiday homes or rental investments. British, European, Australian, and American buyers remain active across all segments.

Emerging markets are also playing a growing role. Indian buyers are increasingly active, particularly in entry-level and midscale condo markets. Buyers from Eastern Europe and Central Asia, including Uzbekistan, are starting to register activity in both the resale and off-plan sectors. Phuket also attracts long-stay families and digital professionals seeking a combination of lifestyle, schooling, and remote work capability.

Source: Bangkok Post – “Phuket housing market still robust”, Jan 2024: In 2023, Russians accounted for around 70% of all foreign residential property purchases, leading the post-pandemic surge. Most acquired larger villas with 3 to 6 bedrooms, priced between 20–60 million THB, or condominiums in the 5–10 million THB range. Many relocated with families, prioritising proximity to international schools and amenities over sea views.

Chinese buyers were the second-largest group, generally favouring short-stay or holiday-use condos. Europeans ranked third, typically seeking spacious homes in low-density projects with rental flexibility.

This 2023 buyer segmentation laid the foundation for the strong 2024 sales cycle, influencing new supply design, pricing strategies, and development location choices.

Phuket and the Rise of Remote Buyers

With its superb connectivity, Phuket has directly benefited from the rise of remote-working and part-time resident buyers. Some professionals work during the week in cities such as Singapore, Hong Kong, or Bangkok, and fly to Phuket on weekends, treating the island as a home base. Others live in Phuket year-round while running global businesses or working remotely.

The island’s reliable infrastructure, international schools, high-speed internet, and expanding wellness and co-working amenities support this lifestyle. These buyers typically favour villas or larger condominiums that offer space, privacy, and the ability to work from home, reinforcing Phuket’s role as a long-stay or part-time residence rather than just a holiday destination.

Location Trends Across the Island

The traditional centres of luxury real estate in Phuket remain concentrated along the west coast. Kamala, Surin, Bang Tao, and Layan are among the most prestigious villa locations, while Patong, Kata, Karon and Rawai also remain popular for condominiums and entry-level second homes.

However, rising land prices, infrastructure expansion, and proximity to international schools have pushed buyer demand inland. Areas like Sri Sunthorn, Phru Champa, Thep Krasattri, and Bang Jo – all part of Thalang District – are seeing extensive new development, particularly in the mid to upper villa segment.

With Phuket spanning just 48 km north to south, even inland properties are within a 15–30-minute drive of the beach, making them increasingly viable for lifestyle buyers prioritising space, privacy, and access to daily amenities.

Notable Areas for Luxury Property in Phuket

Phuket’s luxury property market is closely tied to geography, with premium real estate consistently focused along the island’s west coast. Areas such as Kamala, Surin, Bang Tao, and Layan have long been established as high-end zones due to their proximity to beaches, scenic views, and access to international-standard amenities.

Surin Beach on Phuket’s west coast – one of the island’s most established luxury villa locations.

The stretch around Kamala’s Millionaire’s Mile remains Phuket’s most famous ultra-luxury enclave, home to some of the island’s most prestigious villas with expansive sea views and gated privacy. However, top-end residential development is no longer confined to Kamala. Phuket’s most expensive villas are now found across several high-value locations, including Bang Tao, Layan, Laem Son, Cape Yamu, the Surin headlands, and Ao Po. Pricing at the top end can exceed $20M USD for sprawling villas in prime positions close to the ocean.

See our full guide to Phuket’s top luxury areas for a detailed breakdown by location.

The Expansion of Phuket’s Property Market into Inland Areas

As premium coastal land becomes increasingly scarce and expensive, developers are shifting inland, targeting larger sites near schools, wellness hubs, and transport routes. This inland push has created a wave of new villa projects designed to appeal to long-stay families and lifestyle-driven buyers.

Buyers are drawn by larger plots, lower density, and improved access to amenities. Projects such as Tri Vananda and Botanica Wisdom reflect this shift, offering master-planned, wellness-integrated villa estates near UWC International School and Thanyapura Health Resort.

Demand is being driven by:

- Families relocating to Phuket full-time

- Remote professionals seeking home-office flexibility

- Buyers priced out of west coast beachfront zones

- Investors looking for long-term appreciation in lower-density neighbourhoods

The Rise of Branded Residences in Phuket

According to C9 Hotelworks, branded residences now account for nearly 20% of Phuket’s total residential inventory. These professionally managed properties, often in partnership with major hospitality groups, appeal to buyers looking for reliability, design quality, and ongoing services.

Notable projects include:

- The Standard Residences in Bang Tao

- Tri Vananda in Thep Krasattri

- Multiple Banyan Tree-branded villa clusters near Laguna Phuket

Buyers are drawn to:

- Turnkey ownership and maintenance support

- International brand credibility

- Wellness and lifestyle integration

- Stronger rental management structures

As Phuket transitions from a tourism-led economy to a multi-use island with residential and lifestyle appeal, branded residences are accounting for an increasing proportion of supply.

Recent Market Snapshot – Q1 2024

According to Sopon Pornchokchai of the Thai Real Estate Research and Valuation Centre (Source: Star Media), Q1 2024 saw the launch of 25 new developments, introducing over 4,000 units valued at 54 billion THB. Most were vacation condominiums in Thalang District, averaging 13 million THB per unit.

C9 Hotelworks noted that resale activity surged during the same period. From January to April 2024, resales accounted for 68% of all transactions, and 70% of single-family home sales. While condominiums continued to sell well, average sales prices fell slightly due to increased activity in the lower end of the resale market.

Phuket’s total project inventory now exceeds 72,000 units, of which about 10,000 remain available for sale. Developers are increasingly competing with their own resale supply, putting pressure on pricing for new launches.

Post-Pandemic Surge and 2023 Record Sales

Phuket’s 2023 property market marked a historic rebound. According to CBRE, over 400 resort villas were sold during the year, quadrupling the pre-pandemic average. Condominium transactions also reached record highs, with more than 2,000 units sold.

This sharp increase was partly driven by the release of pent-up demand. Travel restrictions in 2020–2022 had delayed many intended purchases, particularly from foreign buyers unable to enter Thailand. Phuket’s recovery began earlier than most resort markets, thanks to the Sandbox program launched in July 2021, which allowed vaccinated international travellers to enter Phuket without quarantine. The initiative kickstarted a wave of demand, particularly for upscale properties, and highlighted a significant shortfall in supply.

According to the Real Estate Information Center (REIC), villa sales in 2022 increased more than fourfold compared to the previous year, with most of the surge concentrated in the second half. This momentum carried into 2023, setting the stage for a record-breaking sales cycle. Once borders reopened, the market saw a surge of previously deferred transactions, especially in mid to high-end villas.

2024 Year-End: Setting New Sales Records

According to Knight Frank Thailand, 2024 was the strongest year for Phuket real estate in over a decade. Condo supply rose by 148% year-on-year with over 10,400 units launched. Villa supply also expanded sharply with 1,263 new units, marking a 51% increase from 2023.

Sales reflected this growth: 6,156 condos were sold (up 60% year-on-year) compared to 573 villas (up 18%). Notably, condominium growth outpaced villas by a factor of three, driven by price accessibility, developer incentives, and rental demand.

Sales were concentrated in a handful of key zones. For condominiums, Bang Tao accounted for 68% of all transactions, followed by Layan (11%), Patong (8%), Naiyang (7%), and Rawai (6%). Villa sales were strongest in Cherng Talay (27%), Phru Champa (19%), and Bang Tao (18%), with additional activity in Bang Jo (8%), Layan (6%), and Kamala (4%). This highlights the west coast’s ongoing dominance while confirming growing inland momentum in areas like Phru Champa and Bang Jo.

Average condo prices held steady at around 140,000 THB per square metre (source Knight Frank). Villa prices increased as buyers favoured larger plots and more functional living layouts. Based on the extensive inventory of Charlesdel, villa pricing in Phuket currently ranges from around 4 million THB at the entry level to over 700 million THB for the most exclusive sea view estates.

Updated Section: 2025 Outlook: Legal Clarity and Global Volatility

Lack of clarity over foreign ownership structures, global market uncertainty, and economic performance are the key themes shaping Phuket’s 2025 outlook.

Since early 2024, Thai authorities have intensified enforcement of nominee company restrictions. Foreign buyers can still acquire property via Thai companies, but those companies must operate as legitimate, income-generating businesses with properly compensated Thai shareholders who are not nominees and have a genuine stake in the business.

As reported in the Bangkok Post on 28 May 2025, Deputy Commerce Minister Napintorn Srisanpang is pushing for a new law that would further tighten restrictions by classifying nominee-related activity as a financial crime.

In June 2024, the Thai government also proposed two significant reforms that could reshape foreign property ownership:

- Extending lease terms from 30 years to 99 years

- Raising the foreign ownership quota in condominiums from 49% to 75%

While both proposals were widely welcomed, particularly by the real estate sector and those advocating for increased foreign investment, they have also faced resistance from groups seeking to preserve restrictions on foreign land ownership. The reforms remain under review, and it is still unclear whether they will be enacted into law.

At the same time, many prospective foreign investors for landed properties are finding the current legal environment confusing and difficult to come to terms with. For years, it was widely accepted that a freehold villa, or land, could be purchased through a Thai company, often with local shareholders arranged via legal or accounting firms. That assumption no longer holds true, leading to a complete lack of clarity and hesitation among buyers.

Some are re-evaluating their plans entirely, while others are adopting a wait-and-see approach, hoping that the Thai government will move forward with legal reforms that would offer clearer and more secure ownership paths for foreigners.

Logic would suggest that if authorities are effectively eliminating the use of corporate holding structures for villa ownership, some form of alternative will need to be offered, otherwise, a significant stream of potential foreign investment risks being lost. Whether such reforms materialise remains to be seen, and for now, that uncertainty is precisely why many prospective buyers are choosing to wait.

On the economic front, global macro uncertainty deepened in early 2025. Even before the implementation of aggressive new U.S.-led tariffs in April, the international climate was already volatile due to the unconventional approach of the U.S. administration, including its open disregard for institutional norms such as Supreme Court rulings and central bank independence, and its apparent creation of geopolitical policy on the fly.

Thailand currently faces a baseline U.S. tariff of 10%, which is set to rise to 36% if a new agreement is not reached before the moratorium expires in July (source: Reuters, 20th May 2025). These tariff pressures have been the most significant factor behind Thailand’s downgraded GDP outlook for the year, as well as similar contractions predicted in countries across the world. Thailand’s National Economic and Social Development Council (NESDC) downgraded its 2025 GDP forecast from 2.8% to 1.8% on 19 May, citing the impact of tariffs and growing global trade uncertainty (source: Bangkok Post, 19 May 2025).

However, judging by current forecast levels, this is unlikely to materially affect property demand in Phuket. The buyer base is dominated by high-net-worth individuals and lifestyle-driven investors, who are generally less sensitive to short-term economic shocks. As long as international travel remains open and tourism flows continue, demand for villas and high-quality condominiums is expected to remain resilient.

The more relevant risk is domestic: the key concern for Phuket is not an immediate reduction in demand, but the potential knock-on effects of fiscal tightening, particularly if infrastructure investment is delayed or scaled back due to lower government revenues.

For a deeper analysis see our report: Phuket Property in 2025: Tariffs, Economic Shifts, and Legal Uncertainty

Infrastructure and Long-Term Investment Confidence

The government of Thailand has firmly demonstrated its long-term commitment to supporting island infrastructure, as evidenced by the following projects:

- The Kathu–Patong tunnel, designed to ease west coast traffic

- Phuket International Airport expansion and a proposed second airport in Phang Nga

- The Phuket Light Rail Transit (LRT) project (planned)

- The new Bumrungrad International Hospital near Mai Khao

- Expressway and digital infrastructure upgrades across the island

- Water security efforts, including pipelines from Phang Nga

However, rapid development in areas like Cherng Talay and Bang Tao has placed increasing pressure on local infrastructure. Land prices have risen sharply, traffic congestion has worsened, and water scarcity has become a growing concern, particularly during periods of low rainfall. Greater reliance on groundwater wells and tanker deliveries has become common in high-demand zones during peak season.

In response, local authorities have initiated key infrastructure upgrades, including a new waste management facility and expanded water pipeline networks connecting to Phang Nga. These projects are designed to alleviate pressure on local utilities, improve sustainability, and support the long-term viability of high-demand residential zones.

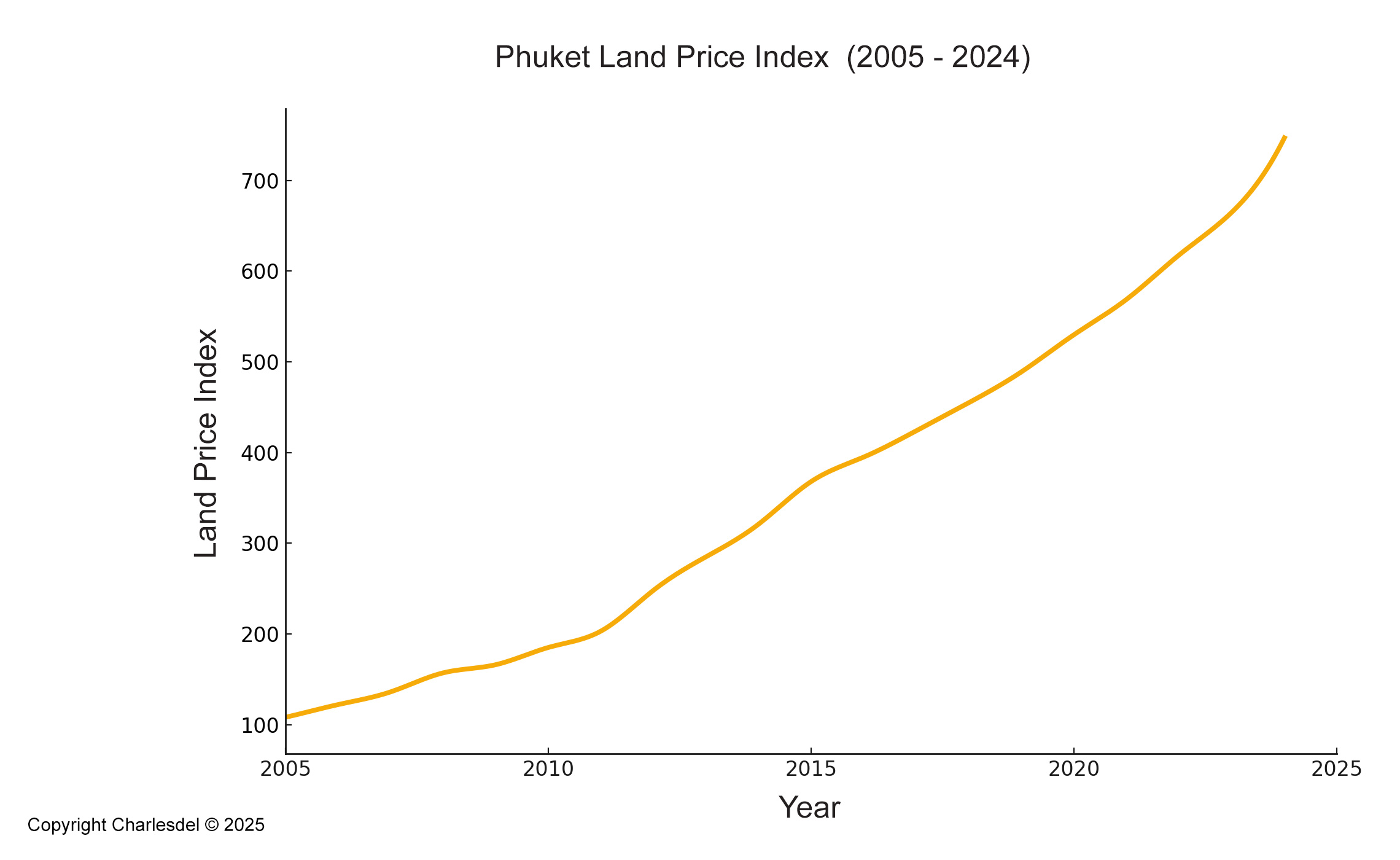

Consistent Long-Term Price Growth

Phuket’s land prices have increased by more than 600% since 2005, based on data from the Thai Real Estate Research and Valuation Centre. While there is no unified index for villa pricing, in part due to the prevalence of company-based transfers, land values across the island provide a reliable benchmark for tracking property prices. Because land accounts for a large share of total development cost, price movements in land are closely reflected in the pricing of completed properties throughout the market.

Prices rose consistently through the global financial crisis, post-COVID recovery, and the Ukraine War & Inflation Spike in 2022. This consistent long-term growth in the face of global crises reflects the cash-driven, tourism-led nature of the Phuket market, underpinned by strong infrastructure – a structure that has repeatedly insulated it from external financial shocks:

Phuket Land Price Index (2005–2024). Source: Thai Real Estate Research and Valuation Centre.