Palma, Mallorca – What Defines the Property Market

Palma is the largest submarket of Mallorca, accounting

The most important enabler for real estate development in any resort destination is infrastructure, and most specifically connectivity. Koh Samui International Airport was opened in 1987, constructed and operated by Bangkok Airways. Following accessibility by international flights, the island’s property market has been gradually developing ever since. Although Phuket’s international airport opened just three years earlier, it already enjoyed easier mainland access via the Sarasin Bridge, which opened in 1967.

The point is this: the property market in Koh Samui has developed steadily since gaining air connectivity, transforming from a backpacker destination into a globally recognised luxury resort and real estate investment centre. This development has been slower than Phuket, largely because the island was slower to gain connectivity, and later again to build out the infrastructure needed to support the evolution of the property market.

As with Phuket, the driving force behind Koh Samui’s property market is tourism. Most investors first visit the island as holidaymakers, get familiar with the environment, and later choose to purchase a property – sometimes remotely, based on their experiences on the island. It’s rare for an investor to buy without having visited first. In 2023, the island welcomed over 3.5 million visitors, with a near-equal split between domestic and international arrivals (source: C9 Hotelworks, June 2024). This marks a clear shift from the pre-COVID era, when the vast majority of arrivals were from overseas.

Much of the recovery following COVID-19 was led by domestic tourism. Airport arrivals recovered to 94% of 2019 levels, while hotel guest registrations actually surpassed 2019 figures by 1.5 times, driven largely by ferry-based travel from the mainland. New regional routes, such as Scoot’s service from Singapore, are helping to diversify international demand. Meanwhile, the planned cruise terminal and future expansion of Samui International Airport reflect a long-term commitment to positioning Samui as a premium destination.

The market rebounded quickly after the global disruptions of the pandemic, highlighting its underlying resilience. Initiatives like Phuket’s Sandbox programme helped sustain demand during challenging periods and introduced the islands to a new segment of travellers, particularly domestic visitors who may not have previously considered Samui or Phuket for extended stays or property investment.

Buyers in Koh Samui tend to be high-net-worth individuals, second-home buyers, expats, and lifestyle-driven investors. Foreign buyers dominate the market and are typically cash purchasers, due to the inability of non-Thai nationals to access local mortgage finance. The same applies to Thai investors, who are also typically high-net-worth individuals. In fact, buyers from Thailand often skew even more heavily toward the upper end of the market, with a stronger presence in the luxury sector and less reliance on credit than is typical in the domestic property sector. This makes the market less sensitive to global interest rate cycles and insulates it from many of the typical credit-driven downturns seen elsewhere.

COVID-19 also contributed to a rise in Thai investors purchasing property on the island. While the majority of residential property transactions involve foreign nationals, Thai demand has remained strong post-COVID, mirroring the broader shift in tourism patterns.

Note: Throughout this article, when we refer to the property market on Koh Samui, we are talking about investment-grade inventory appealing to holidaymakers and lifestyle buyers, and excluding low-cost accommodation such as worker housing or basic bungalows aimed at the local market.

Koh Samui’s property market has always been dominated by villas. While there are a reasonable number of leasehold apartments and few freehold condominium developments on the island, the proportion of total stock made up of villas is far greater than in Phuket. Buyers in Samui typically value space, privacy and views, hence the market’s focus on detached pool villas rather than dense apartment blocks.

Condominiums and apartments can be acquired for as little as a few million baht. Entry-level villas in Koh Samui can be found from as little as THB 5 million, occasionally even with a private pool. Properties at this level are typically leasehold and may be offered on a single 30-year term. Between THB 6–15 million, buyers can expect well-designed garden villas, often single-level Bali-style or modern contemporary homes. At around THB 15 million and above, villas with partial sea views become available, although many properties marketed as “sea view” may offer only a narrow or distant glimpse.

Absolute beachfront properties are rare and command a significant premium, with starting prices from around THB 60 million. At the very top of the market, Samui’s most exclusive villas are priced between USD 8–10 million, lower than the highest tiers in Phuket, where ultra-prime homes can exceed USD 20 million.

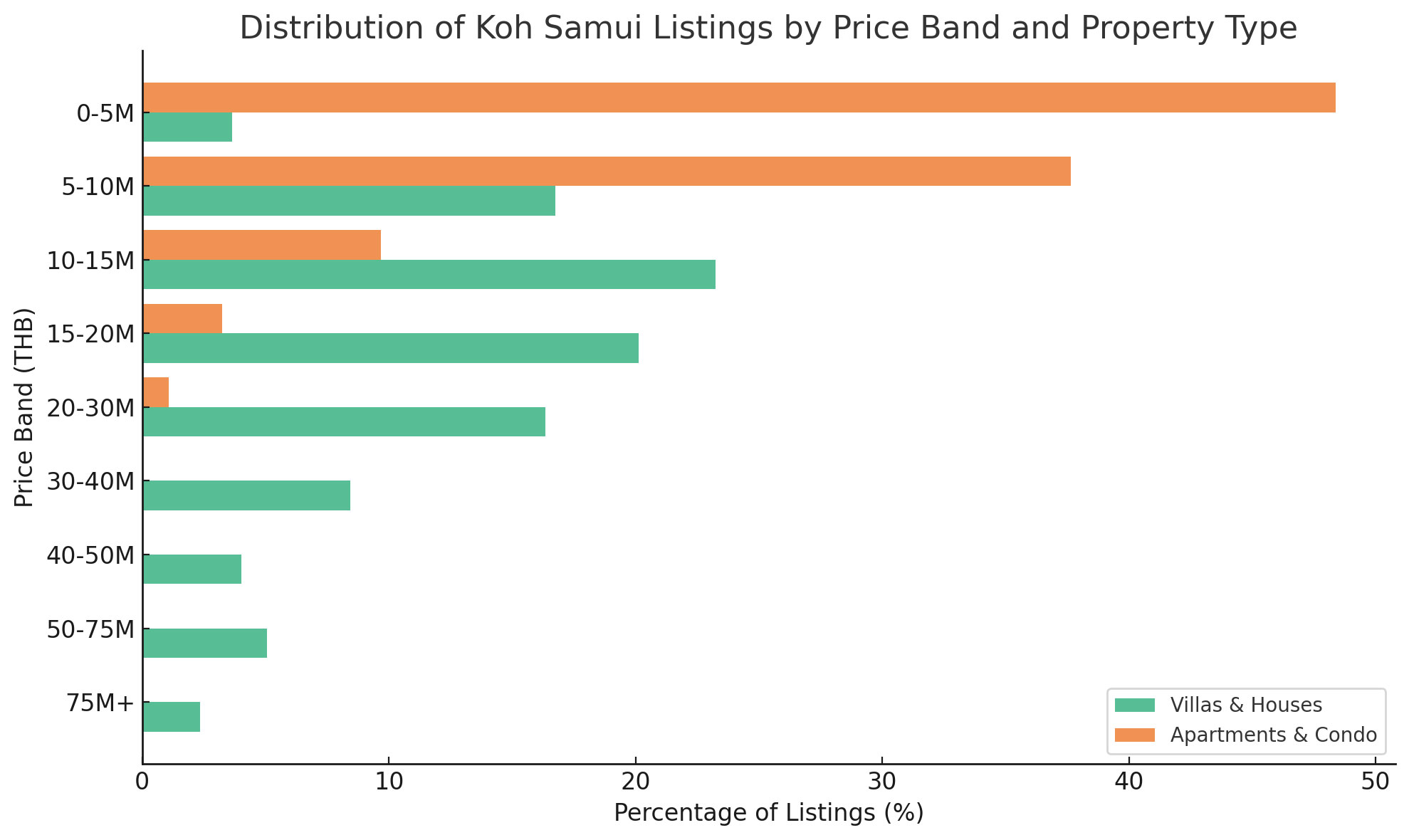

Villas and Houses: The most common price band is 10–15 million THB, followed by 15–20 million THB, and then 5–10 million THB. This may seem surprising given that the average listing price for Koh Samui villas and houses is ฿30.5 million, but—as is common in many property markets—the mean is heavily skewed by luxury listings. At the top end of the market, there are a significant number of exclusive villa estates priced between ฿200–400 million, which inflate the overall average despite representing only a small share of total inventory.

Apartments & Condos: By far the most common price band for apartments and condominiums is 0–5 million THB, with nearly half of all listings falling within this bracket. Next is 5–10 million THB, which accounts for over a third of available listings, followed by 10–15 million THB, with just under 10%. Beyond this point, there are no significant numbers of listings, highlighting the limited presence of high-end or luxury apartment stock in Koh Samui.

| Price Band (THB) | Villas & Houses (%) | Apartments & Condos (%) |

|---|---|---|

| 0–5M | 3.64 | 48.39 |

| 5–10M | 16.75 | 37.64 |

| 10–15M | 23.25 | 9.69 |

| 15–20M | 20.13 | 3.23 |

| 20–30M | 16.36 | 1.08 |

| 30–40M | 8.44 | 0.00 |

| 40–50M | 4.03 | 0.00 |

| 50–75M | 5.06 | 0.00 |

| 75M+ | 2.34 | 0.00 |

Note: Data based on our own analysis of 863 live listings on Thailand-Property, captured on 27 July 2025. The average listing price for villas and houses was ฿30.5 million, with a median of ฿17.2 million. For apartments and condos, the average was ฿6.5 million and the median was ฿6.6 million. View full price band breakdown here.

Koh Samui offers excellent value for money compared to both Phuket and international resort markets, particularly in terms of what buyers receive at each price point and on a per square metre basis.

At the entry level, buyers can purchase an apartment or condominium for as little as a few million baht. In contrast, in Mallorca it is difficult to find an apartment for less than €200,000 – approximately 7.4 million baht (source: Charlesdel).

Within Thailand, the most comparable market is Phuket, given its tropical island appeal and well-developed lifestyle infrastructure. While entry-level apartments in Phuket may not be priced much higher than in Koh Samui, the difference becomes more pronounced in the villa market.

In Koh Samui, sea-view villas can be acquired from around 15 million baht. In Phuket, these will usually be priced at 30 million baht or more. Samui garden villas are usually priced below 15–20 million baht, unless they are located right next to the beach. In Phuket, by contrast, it is quite common for inland villas with no view to be priced over USD 1 million. This relative price difference reflects Koh Samui’s less mature property market, lower land prices, and limited presence of branded developments or widely recognised developers.

Koh Samui has not only been predominantly a villa market, but for many years, the majority of villa purchases by foreign buyers were facilitated through Thai limited companies. While this structure was long considered a practical workaround to the restrictions on foreign land ownership, it has come under increased scrutiny in recent years. With strict enforcement of the laws surrounding nominee shareholders and foreign-controlled company structures, it is now prohibited for a Thai company to be set up solely to hold land on behalf of a foreign buyer. The required 51 percent Thai shareholding must consist of genuine shareholders, and the company must operate as a legitimate, income-generating business – typically a property rental enterprise. The medium to long-term impact of this change on the villa market remains uncertain.

Foreigners are not permitted to own land freehold in Thailand, and this applies across Koh Samui. Most villa purchases are therefore structured either as leasehold agreements or via a Thai limited company. In 2024, the government began a strict crackdown on nominee shareholder structures, enforcing rules that had historically been loosely applied. Source: Bangkok Post, 28 May 2025, Deputy Commerce Minister Napintorn Srisanpang is advocating for legislation that would classify nominee-based land ownership structures as a financial crime, signalling the possibility of even stricter enforcement measures ahead.

As a result, many developers have shifted to offering leasehold villas, particularly in the THB 5–12 million range. These leaseholds are typically sold on a single 30-year term, with pricing adjusted to reflect the limited tenure. However, a large proportion of resale villas currently on the market are already held via Thai companies. In these cases, the land (and sometimes the villa itself) is owned by a company, which is usually included in the sale. This creates a major complication for prospective buyers. With the recent legal crackdown, many are hesitant to proceed, unsure whether they can lawfully acquire the company or maintain the structure. At the luxury end of the market, the financial viability of operating a fully compliant company – assuming a genuine business purpose such as rental income – can still make the structure workable. The same applies where multiple properties are consolidated within a legitimate rental business.

In June 2024, the government of Thailand announced its intention to implement two proposals that would significantly improve foreign ownership options and stimulate investment: extending lease terms from 30 to 99 years – applicable to both villas and apartments – and increasing the foreign quota in freehold condominium developments from 49% to 75%.

As of mid-2025, the proposals remain under review, and it is still uncertain whether they will be enacted.

See Our Foreign Ownership Guide for Property in Thailand

As outlined in the introduction, connectivity has always been the foundation of Koh Samui’s property market evolution, but the island has consistently played catch-up with Phuket. While Phuket benefitted early from road access via the Sarasin Bridge and developed a broader infrastructure base, Samui has followed a slower but steady trajectory. Today, Phuket still holds the advantage in terms of international schools – around 16, depending on definition, versus 6 in Samui – along with a wide range of shopping centres compared to just a handful on Koh Samui, and better hospital coverage. These factors support long-stay expats and family buyers.

That said, Samui has made meaningful progress since gaining municipality status in 2012. Road upgrades, expanding ferry links, and the planned airport expansion all point to continued development. In terms of air connectivity, Koh Samui is now relatively well connected, with regular flights to Bangkok and select international destinations including Hong Kong, Singapore, and Kuala Lumpur, though its overall network and flight frequency remain more limited than Phuket’s. For many lifestyle buyers, Samui’s balance of improving services and preserved natural charm remains a key part of its appeal, especially for those prioritising privacy over convenience.

Two upcoming infrastructure projects are set to shape Koh Samui’s long-term development. The first is a new international cruise terminal, scheduled for completion by 2032. Construction is expected to begin in 2029, with the goal of attracting major cruise ships from Singapore, Pattaya, and other Gulf of Thailand destinations. The second is a proposed bridge to the mainland (source: The Nation, July 2024), backed by the Expressway Authority of Thailand. The four-lane structure would span approximately 25 kilometres, linking Samui with Nakhon Si Thammarat province. Construction is expected to begin in 2029, with opening currently targeted for 2033. Once complete, the bridge would significantly improve connectivity to the island, providing land access similar to that enjoyed by Phuket.

Even though both islands offer broadly similar property types, the diversity and availability of options between Koh Samui and Phuket are markedly different. Due to stricter zoning and building regulations, there is significantly less land available on Samui for the development of freehold condominiums. Currently, Samui has only two notable mid-market freehold condo projects – Anava and Wing Samui – and just one branded residential development on the market: The Estates by Four Seasons, which opened over a decade ago. In contrast, Phuket has an abundant supply of freehold condominiums across all price points, along with a wide selection of branded residential properties. Another major difference is the widespread availability of renewable leasehold properties – both villas and apartments – offered by well-established and recognised developers. These are limited in Koh Samui but prevalent in Phuket. The credibility and reputation of the developer are critical in these cases, as the long-term security of lease renewals remains a grey area under Thai law.

The northeast of the island, including Chaweng, Choeng Mon, Bo Phut and Plai Laem, is the most developed region for both tourism and property. This part of Samui developed first due to its proximity to the island’s longest and most commercially valuable stretch of beachfront at Chaweng. As Chaweng became the island’s premium tourist hub, real estate development naturally expanded into the surrounding areas. The second most popular area for property investment is Lamai, which also serves as the island’s second-largest tourist centre. Other buyers favour quieter parts of the island, such as Maenam, Lipa Noi or the south coast, which offer more space, privacy, and a less developed feel.

Within the northeast, areas such as Choeng Mon and Plai Laem offer access to some of the best beaches, hillside views, and proximity to the airport. Bo Phut includes Fisherman’s Village, known for its restaurants, open-air shopping and family appeal. Chaweng Noi and Lamai offer hillside views and access to good beaches, with the surrounding areas of Hua Thanon and Laem Set offering lower-density beachfront options.

Bang Por is emerging as a new focus for development, with its peaceful setting, quality beach, and relative proximity to Maenam.

Bang Por Beach on Koh Samui's unspoiled north-west coast.

The west coast (Lipa Noi, Taling Ngam) is known for its luxury beachfront villas, striking sunsets, and hillside estates with sweeping views of nearby islands and the mainland.

Koh Samui’s less developed market offers exceptional opportunities for capital gains, particularly in early-stage projects. However, investors should exercise caution, as some projects are by first-time developers who rely heavily on off-plan sales to fund construction.

The highest opportunities for capital appreciation exist in off-plan or under-construction projects, where developers may offer substantial discounts to early buyers. In some cases, it is possible to realise capital gains of 10–15% by completion. That said, there are no guarantees, and buying off-plan requires enhanced due diligence and a clear understanding of the risks involved.

The villa rental market in Koh Samui remains robust, particularly for short-term holiday lets. While Phuket offers a more established rental ecosystem, Samui continues to benefit from growing tourism demand, which supports healthy occupancy levels and rental yields.

Net rental returns of 6% to 8% are achievable for well-located properties that are efficiently marketed and professionally managed. Villas that appeal to the tourist segment and offer strong amenities tend to perform best in the short-term rental space.

Since the inauguration of the new U.S. administration, the policy-led global market volatility in 2025 is plain to see. This reached new heights with the aggressive tariffs announced in April. These actions have not only triggered downgrades to global GDP forecasts but also reduced investor confidence across industries worldwide.

However, the cash-based, tourist-driven resort destinations of Thailand, including Koh Samui, are partially insulated from these downturns due to their higher-net-worth, lifestyle-oriented buyer base and low leverage. History also shows that both Koh Samui and Phuket have consistently rebounded from major global crises, most recently, the COVID-19 pandemic.

That said, it is important to acknowledge the ongoing challenges surrounding villa ownership — both for existing owners holding properties via corporate structures and for prospective buyers seeking long-term security. This remains a concern for Koh Samui’s property market, which has traditionally been dominated by villas and lifestyle-driven buyers. Looking ahead, some form of regulatory adjustment seems not only likely but necessary. The most desirable outcomes would include viable, legally sound structures for long-term villa ownership, along with relaxed zoning regulations to enable more freehold condominium development, conditions that could help attract established developers and branded operators to the island.

Samui’s fundamentals remain strong, underpinned by a resilient lifestyle-driven buyer base and a buoyant rental market. The island continues to attract well-capitalised purchasers who prioritise privacy, natural beauty, and a sense of exclusivity. Provided infrastructure investment continues, and legal frameworks evolve in line with market expectations, Koh Samui is well positioned to remain one of Thailand’s leading resort property markets in the years ahead.

See our properties for sale in Koh SamuiPalma is the largest submarket of Mallorca, accounting

This report covers: Andratx Market Overview Luxury Villa

Why British Investors Choose Pollensa This article is